Chairman, Endeavor Brazil

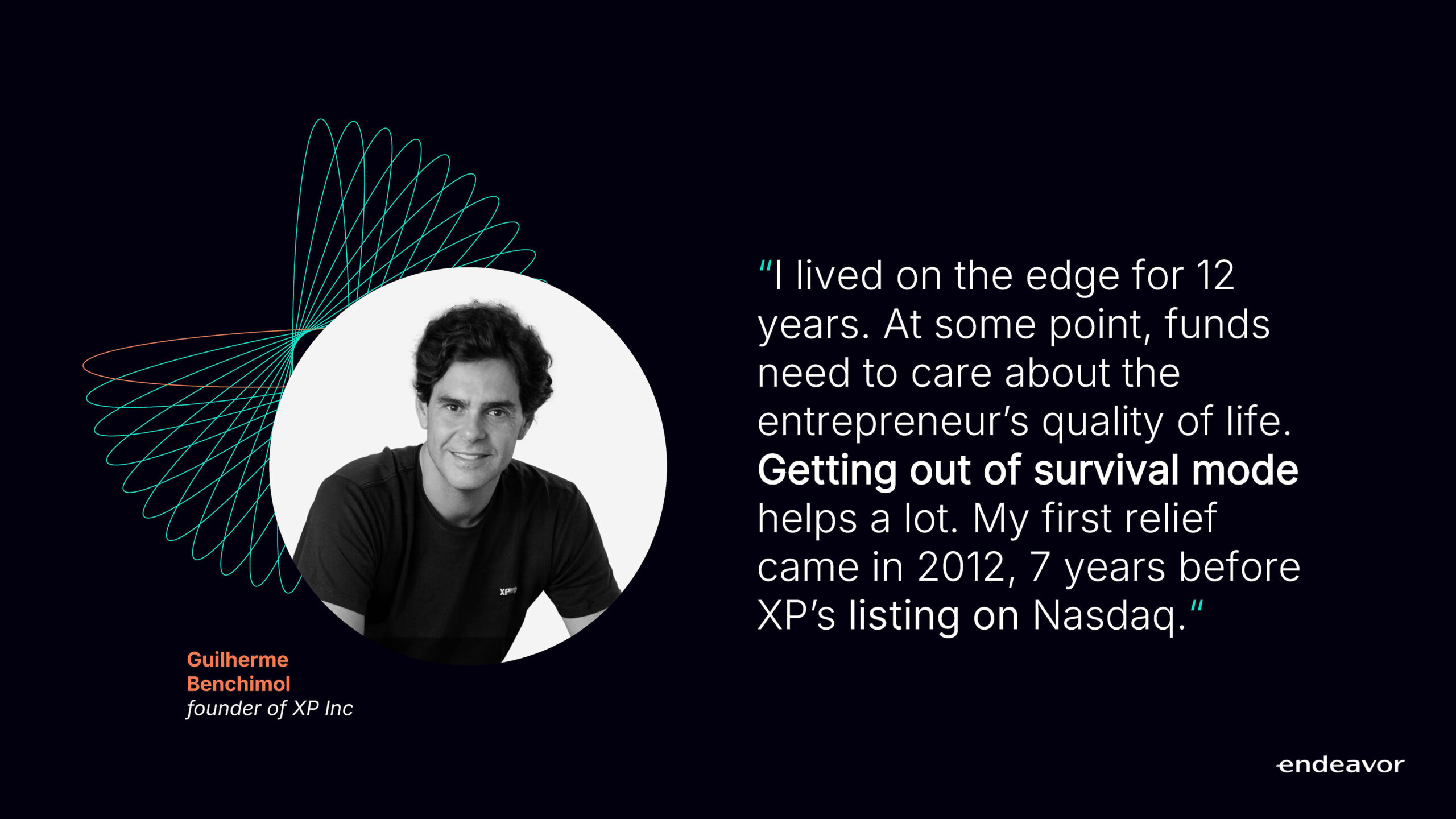

We Built XP to Last Forever

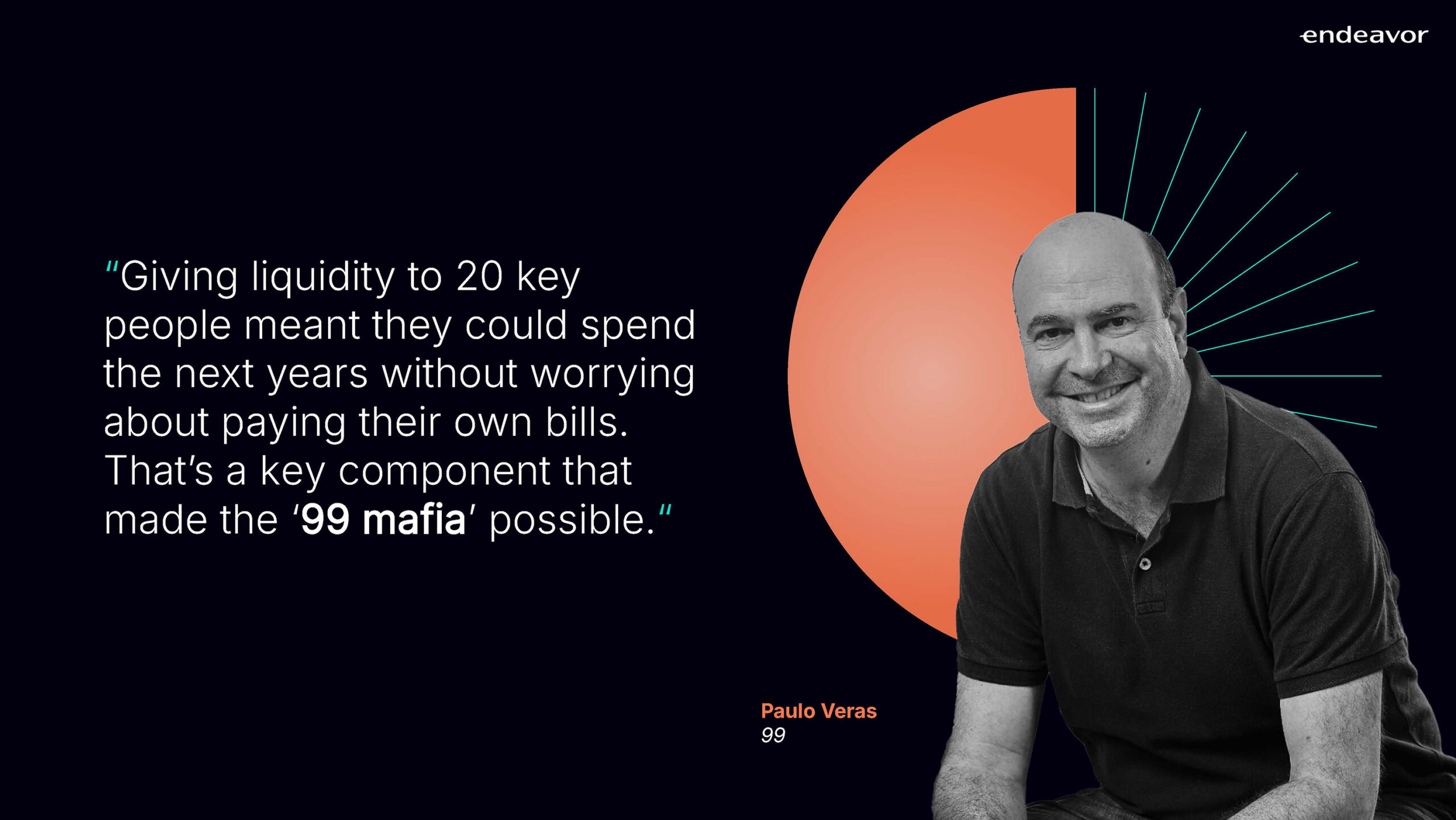

Selling 99 Was The Right Call — And Just The Beginning

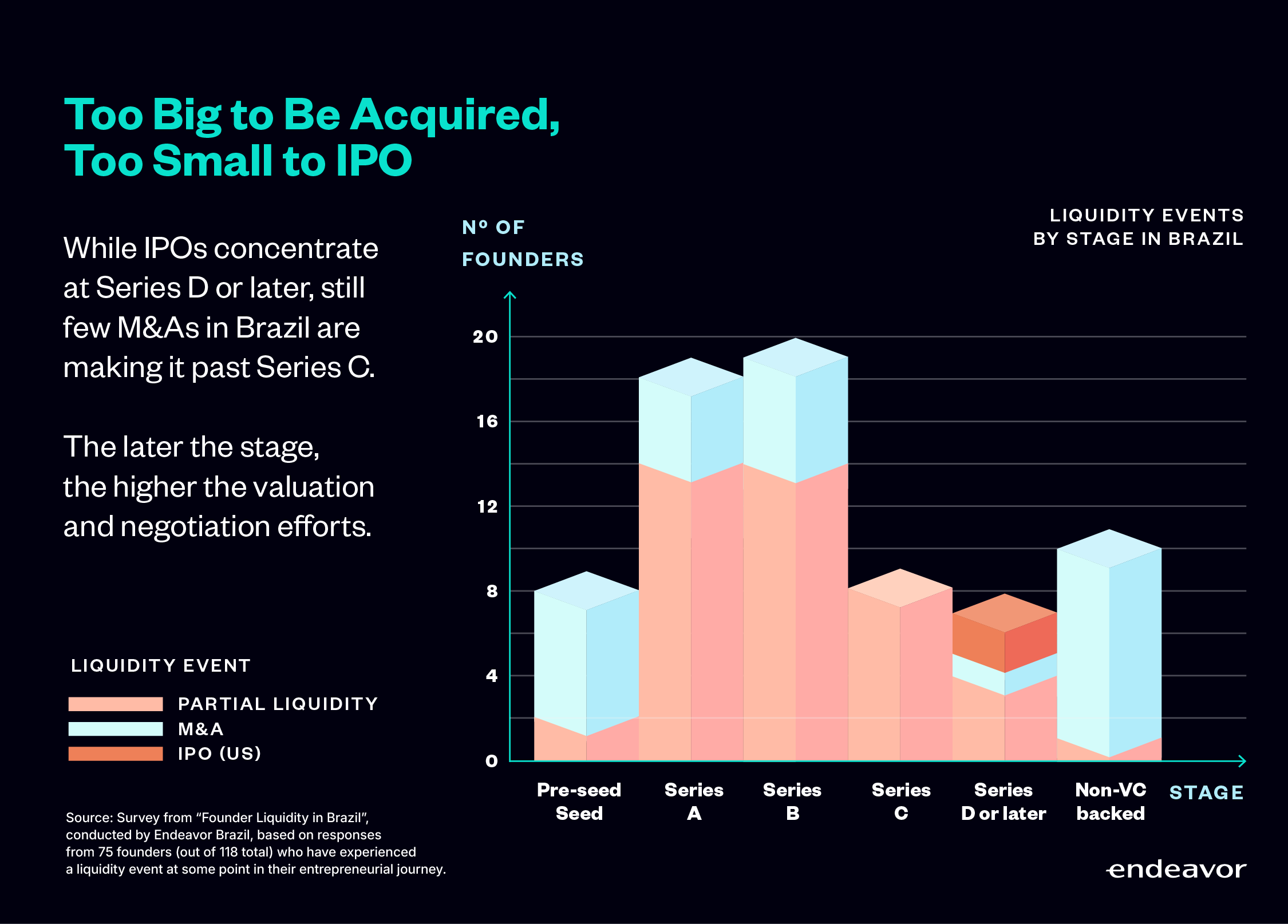

If I Deliver Results, Why Not Do A Secondary?

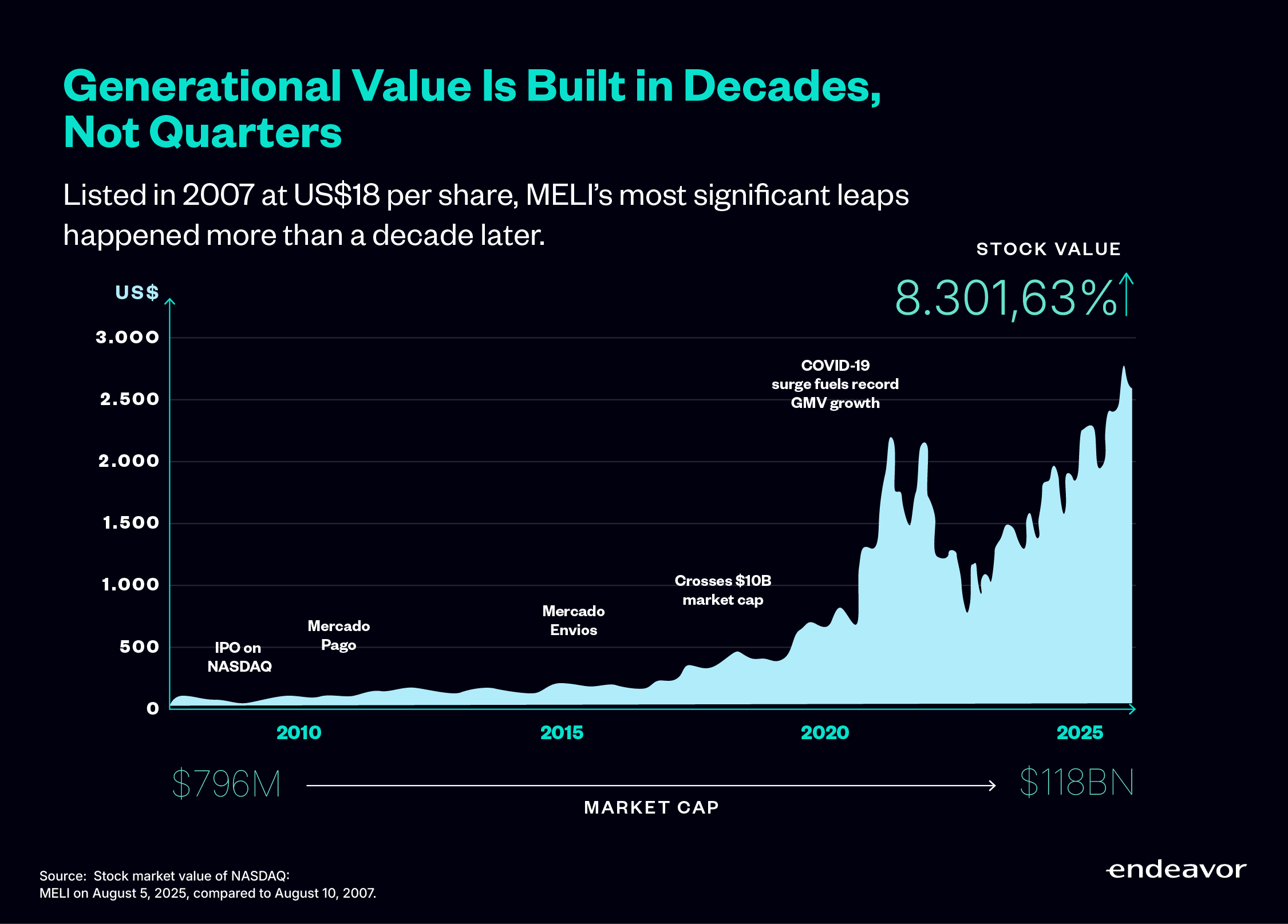

From Hosting to the e-Commerce Giant

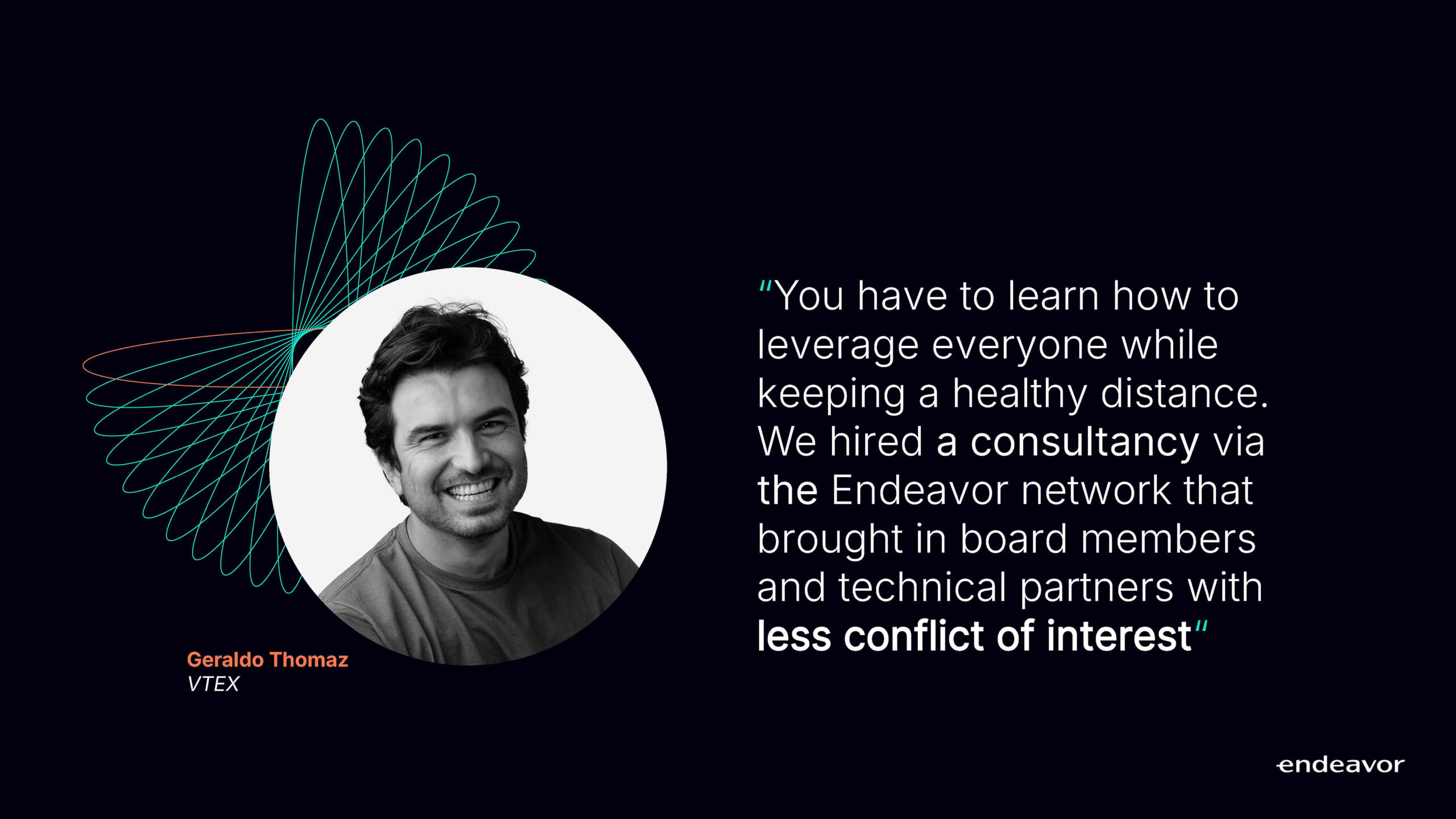

Every Term Was A Building Block For What Came Next

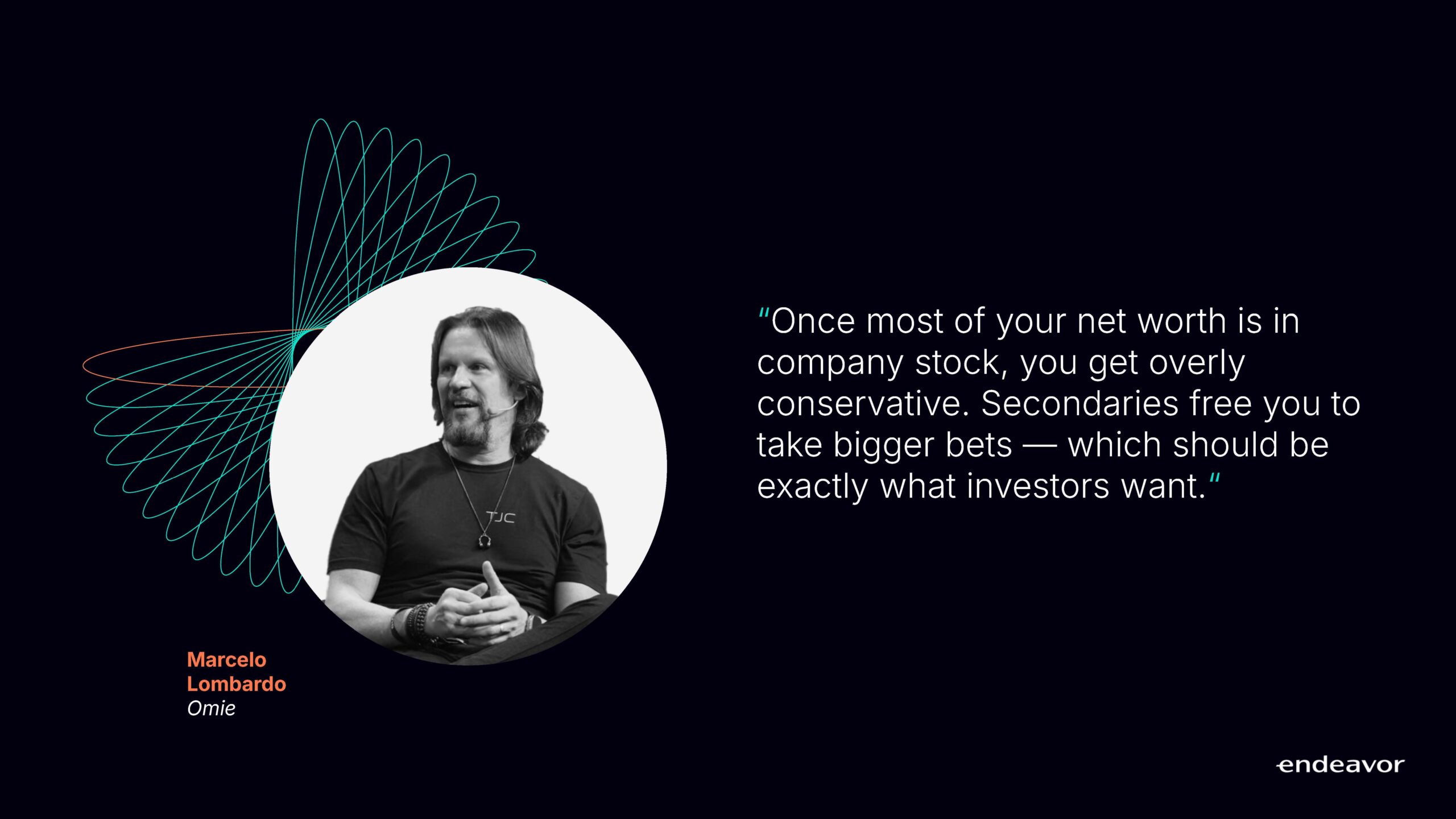

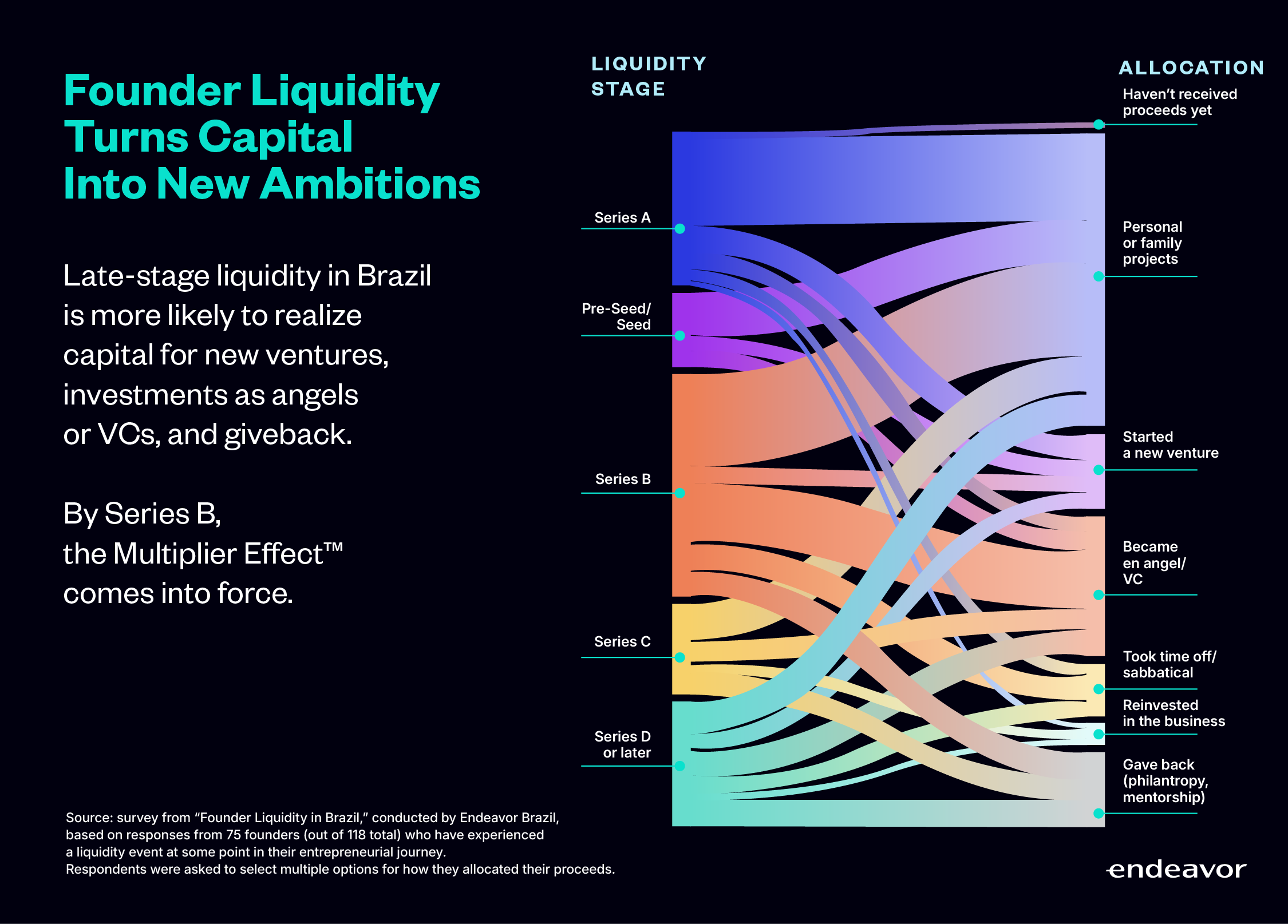

Secondaries Let Founders Keep Dreaming Big

Building Discipline Before Ringing The Bell

My First M&A Was With Myself

What Makes Us Proud Is What Came After the IPO

When Markets Are Uncertain, Fundamentals Lead the Way